Rethinking Retirement: Strategies for Holistic Financial Security

Who said retirement was supposed to be a countdown to just sipping lemonade on the porch? In today's fast-paced world, it's about so much more. It's travel, leisure, hobbies, and yes, even those unexpected costs that sneak up on us. Traditional views of retirement savings? They're evolving, and it's high time we step into the new age of planning for those golden years.

Section 1: Understanding Your Retirement Needs

- Redefining Replacement Rates: A New Reality

- Here's a fun fact: retirement could mean spending more, not less. Shocking, right? But think about it. More free time often equals more expenses, from jet-setting to visit the grandkids to picking up that golf hobby you always swore you'd master. It's clear: the old-school replacement rates don't always cut it. We might need a bigger slice of that financial pie to keep the good times rolling in retirement.

2. The Three-Legged Stool: A Shaky Foundation

- Picture retirement planning as a stool with three legs—Social Security, employer pensions/401(k)s, and personal savings. Now, what happens if one leg is shorter than the others? Spoiler: It's not comfortable! Too many of us neglect that personal savings leg, and stability goes out the window. Time to even things out for a smoother sit, folks!

Section 2: The Role of Social Security

- Alright, let's talk Social Security. It's a safety net, sure, but it's not a hammock. You can't just lay back and relax on Social Security alone. This section is a reality check about what Social Security brings to the table (hint: it's just one dish in a potluck retirement buffet).

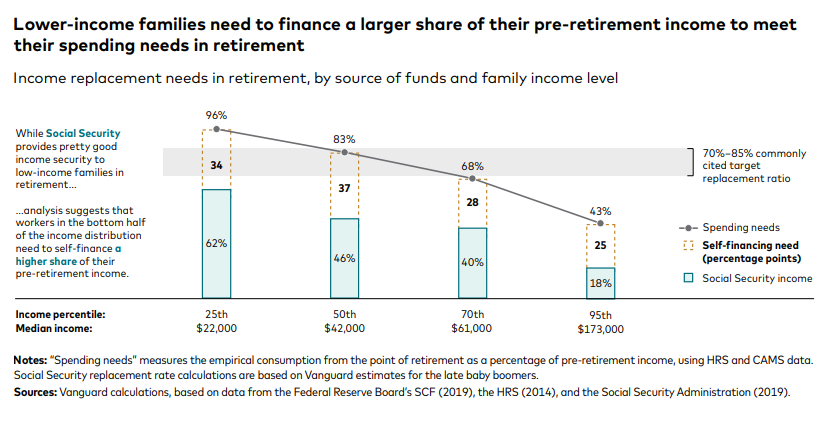

Section 3: The Savings Gap Challenge

- Money talk is tough, especially when we get into the nitty-gritty of income disparities. This part? It's about understanding where you stand and how "sustainable replacement rates" can be your financial GPS, guiding you toward a retirement that doesn't mean choosing between necessities and niceties.

Section 4: Navigating Retirement Realities for Lower-Income Workers

- No sugar-coating here: lower-income workers have a steeper hill to climb. But it's not an impossible hike. We've got practical, doable strategies that can put a summit bid within reach. It's all about knowing the terrain and having the right gear.

Section 5: Innovative Strategies for a Secure Retirement

- Expanding Your Financial Portfolio with Cash Value Life Insurance:

- Cash value life insurance is like the Swiss Army knife of financial planning—so many tools in one handy package. From growing your funds tax-free to borrowing without losing out on interest, and access to your death benefit while you are alive through living benefits, it's a multitasker that deserves some spotlight in your retirement strategy.

2. Understanding Annuities: Predictable, Lifetime Income

- Annuities are the superheroes of the retirement world—rescuing you from the perils of market slumps with the superpower of guaranteed income. Whether it's weathering health storms using income doublers or just securing that steady cash flow, annuities are worth a look in any nest-egg plan.

3. Holistic Planning: Beyond Savings and Investments

- Life's unpredictable. So, a game plan that looks at the big picture is the way to go. We're talking health, hobbies, hidden costs—the works. This approach isn't just about surviving; it's about thriving in your later years.

Section 6: Health and Unexpected Retirement Costs

- If life throws a curveball (read: health hiccups), it pays—literally—to have a financial buffer. Its important to build that emergency fund, so unexpected bills don't derail your retirement train.

Section 7: The Value of Professional Guidance

- Sometimes, we need a hand navigating the maze of retirement planning. Work with a financial coach/mentor, or financial success engineer. They're the experienced guides you want. They’ve work with you to create your personal retirement map, the compass, and have the know-how to help you reach your personal El Dorado.

Section 8: Timing Is Everything: The Sooner, The Better, But It's Never Too Late

Listen, we've all procrastinated at some point, but if you're doing it with your retirement planning, it's time to switch gears. The magic of compound interest is like a snowball rolling down a hill - it needs time to grow bigger. The earlier you start, the more you harness this power. But what if you've hit snooze a few too many times on planning?

Don't beat yourself up; you're not out of the game. It’s true, starting earlier could give your savings more growth muscle, but late bloomers can still catch up. You'll need to be a bit more strategic, perhaps save a larger slice of the pie, and possibly adjust your vision of retirement.

But know this: embarking on a plan now, however late, still puts you leagues ahead compared to leaving it to chance. In the retirement game, having a late plan is your secret weapon against no plan.

Conclusion:

So, here's the real talk—retirement planning is a bit like planting a tree. The best time to do it was 20 years ago. The second-best time? Today. Whether you're an early bird or just waking up to the reality, taking charge of your plan is the ticket to making a difference in your retirement life.

It's about creating a strategy that's not only a safety net but a launchpad for your dreams, ambitions, and peace of mind. Proactive planning is your map, compound interest your vehicle, and resilience your fuel. With these, you're set for a journey toward a destination you deserve.

Let's not mince words: crafting a secure retirement requires effort, consistency, and foresight. But with these powers combined, you're not just waiting for the future; you're building it, brick by financial brick.

Call to Action:

No more sidelines. It's time to step into the retirement planning arena. Whether you’re early to the party or fashionably late, the point is you’re here. Reach out for guidance, upskill your financial literacy, and take the reins. Your future self is counting on you, and honestly, there's no one better for the job.